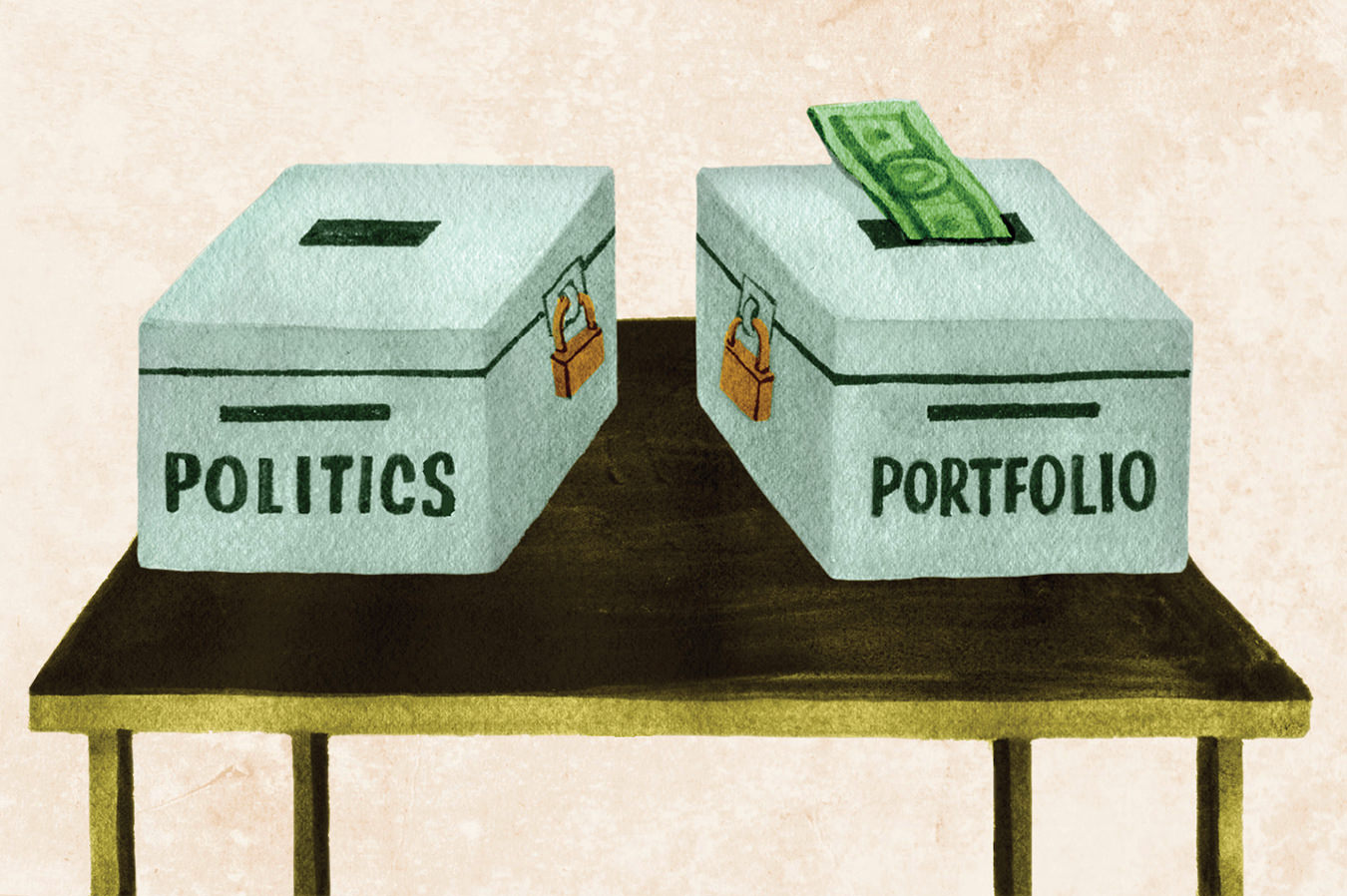

Politics and Your Portfolio

Blame game.

Whoever thought up the “war is good for business” thing might want to check out the action on the Moscow Exchange this year. As the crisis in Ukraine came to a boil at the end of February, investor appetite for Russian equities went into a deep freeze, and the country’s benchmark Russian Trading System (RTS) stock-market index lost 19 per cent in a matter of weeks. As cooler heads prevailed, Russian equities became red hot, with the RTS gaining some 30 per cent since mid-March.

It’s a common pattern. When the barricades go up, stock markets move in the opposite direction; once they come down (via democracy or despotism—money is agnostic), things start looking up. Example: Egypt, whose EGX 30 index sunk fully 44 per cent in the months following the Arab Spring. As order was restored, so too were the gains, and the EGX 30 has recently touched all-time highs.

So politics and profits are joined at the hip—no surprise there. But as capitalism goes global, reading the political tea leaves has become a mission-critical task for many corporations. And it’s not just riot and rebellion you have to watch out for. When your balance sheet depends on the continued goodwill of junta generals or backwater kleptocrats, politics is a game played for high stakes. Just ask Toronto-based Crystallex International Corporation, which found itself on the wrong side of Hugo Chavez’s Bolivarian dream. Or First Quantum Minerals, which is trying to recover $150-million (U.S.) in VAT rebates from Zambia. Or Turquoise Hill Resources, currently embroiled in a dispute over penalties on suddenly disallowed entitlements in Mongolia.

Such threats are not limited to those who dig and drill. As growth in the developed world becomes harder to come by, most of the blue chips that are the go-to investments of the recently- and soon-to-be retired are aggressively pursuing growth in developing economies. Changes in trade regulations, environmental guidelines, or labour law (whether deserved or capricious) can have a significant impact on the bottom line.

What can investors do about such risk? Not much. Forecasting the financial implications of political change halfway around the world is as difficult as guessing what Miley Cyrus will do with her tongue at the next awards show—opinions abound, but the only way to know for sure is to sit back and watch. Instead of sweating the details, perhaps the best solution is the simplest: diversify. Put your eggs in more than one basket, whatever continent that basket may reside, and leave the all-in bets to the poker stars.

That done, you’re free to turn your mind to a more challenging question. As markets slide and shares sink, the temptation to put financial pragmatism over political principle grows ever stronger. As much as we may root for hope and change in Tahrir Square, Lumpini Park, or Maidan Nezalezhnosti, our pensions and our RRSPs have a vested interest in the economic status quo. So how do we square our financial goals with our desire to let freedom ring? Does realeconomik trump political idealism? When it comes time to back either our politics or our portfolios, which box do we mark on the ballot?